.png)

The 340B rebate model is not dead. It is not finalized. It is somewhere in the middle, moving through a federal rulemaking process that will likely produce a new rule sometime this fall. Based on the last runway we witnessed with the rebate model a probable implementation date of January 1, 2027 is possible. If that timeline holds, covered entities have roughly six months to understand what is coming and prepare for it.

The rebate model has been contested terrain since 2024, when several manufacturers attempted to implement rebate-based pricing for 340B on their own initiative. HRSA intervened and established that any rebate model requires agency pre-approval before implementation.

In July 2025, HRSA launched a voluntary pilot program covering up to ten Medicare Part D drugs selected under the Inflation Reduction Act, with a planned launch date of January 1, 2026. HRSA approved a group of manufacturers to participate. Shortly before launch, on December 1, 2025, a coalition of hospitals and hospital associations filed suit arguing the pilot bypassed required rulemaking procedures under the Administrative Procedures Act. On December 29, a federal court halted the pilot, ruling HRSA had not adequately justified the program's departure from the existing upfront discount model.

A federal appellate court affirmed that ruling on January 7, 2026. The parties agreed to dismiss the case on January 12, with HRSA committing to restart the process in compliance with APA requirements.

In February 2026, HRSA published a Request for Information seeking public comment on the design of a new rebate model. That comment period closed in April. On May 27, 2026, HRSA submitted its proposed rebate model to the Office of Management and Budget, formally beginning the pre-rule stage.

.png)

The rulemaking process from this point follows a predictable sequence, though the timing at each stage can vary.

The OMB is now reviewing the proposal to evaluate its economic impact. During this period, stakeholder groups including hospital associations and manufacturers may request meetings with OMB to present their positions. OMB review typically takes 30 to 90 days.

Once OMB clears the proposal, HRSA publishes it in the Federal Register as a Notice of Proposed Rule Making (NPRM). This is when the actual details of the new model become public: which drugs it covers, which entity types are included, how pharmacy and medical claims factor in, and when it would begin. A public comment period of 30 to 60 days follows publication of the NPRM.

After reviewing those comments, HRSA publishes a final rule. Based on what HRSA stated in connection with the original pilot, covered entities are to receive 90 days' notice before any rebate model takes effect. Following that logic and the timeline from last year, a final rule this fall would point toward a January 1, 2027 start date.

.png)

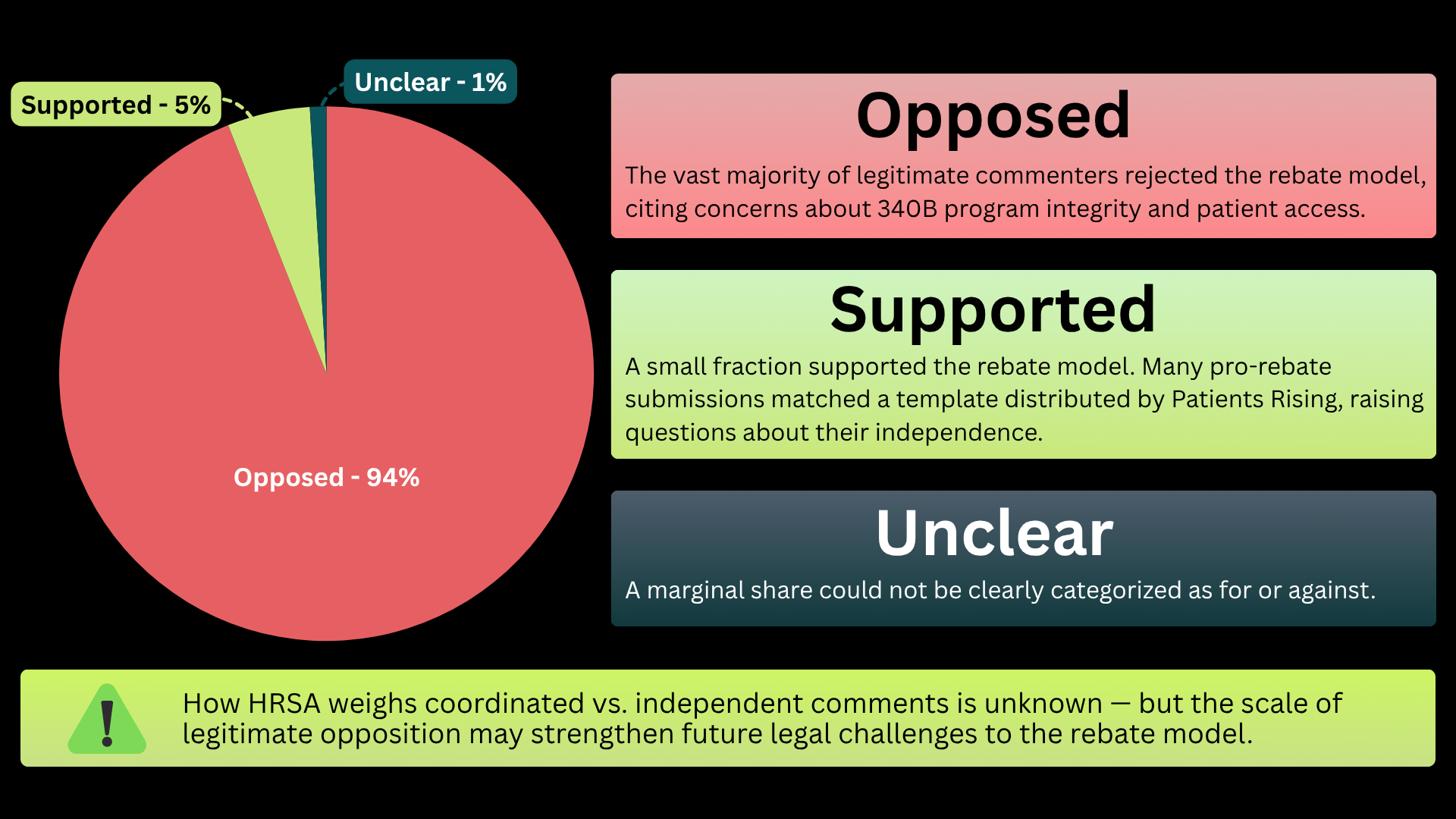

The RFI generated 5,589 total comments, described as the largest response HRSA has received on a 340B-related issue. Of those, approximately 2,500 were made publicly available. Analysis of the public comments found roughly 1,300 to be independently drafted unique submissions. Of those, approximately 94% opposed the rebate model, 5% supported it, and 1% were unclear.

Among the comments supporting the rebate model, approximately 1,200 followed a coordinated template traced to an organization called Patients Rising, which has received pharmaceutical industry funding. These submissions arrived in alphabetical order with identical language, distinguishing them from independently drafted responses.

How HRSA weighs coordinated submissions against unique ones in its rule making analysis is not publicly known. What the record establishes clearly is substantial, widespread concern from covered entities about cash flow impact, administrative burden, operational feasibility, and patient access.

The NPRM will answer questions that cannot be answered today. Specifically: which drugs the new model will cover, whether it applies to all covered entity types or a subset, whether it encompasses pharmacy claims only or medical claims as well, and what the rebate payment timeline and reconciliation process will look like.

Until NPRM publication, planning has to be based on what the IRA MFP rebate process has already revealed about how rebate models function in practice. That preview has not been encouraging in terms of administrative complexity, and it is worth using that experience as a baseline assumption.

Understand your IRA drug exposure now, not after the rule is published. Look at which negotiated drugs your entity dispenses, what your current savings on those drugs look like, and what your cash flow timeline would be if upfront discounts shifted to post-dispense rebates. This analysis will be different for every covered entity, and it takes time to run properly.

Start asking your TPA about rebate submission capabilities. Know what data you can produce today for pharmacy and medical claims, where the gaps are, and what the realistic timeline is for closing them.

.png)

Think through who in your organization would own rebate reconciliation. Submitting claims is one job. Monitoring rebate payments, reconciling what was submitted against what was paid, and chasing missed rebates is a second, ongoing job that does not go away after the initial submission.

RxTrail is running financial impact analyses for covered entities now, before the final rule is published, so that clients have a clear picture of their exposure across both the 2026 and 2027 IRA drug lists. If you want that analysis for your program, reach out.